I am pleased to present the Bank’s Corporate Governance report on behalf of our Board. The report

includes details of how governance underpins our business, and the decision-making as we deliver our

strategy and create long-term value for our shareholders.

The Bank recognises corporate governance as a dynamic concept, supported by a framework of rules,

systems, and processes adopted by the organisation. Good governance facilitates effective management and

enables the Bank to maintain a high level of business ethics. The Board sets the example for employees

of the Bank by implementing the highest standards of business ethics and corporate governance. We

maintain a zero-tolerance approach to bribery and corruption, and expect all employees to comply with

applicable laws, regulations, and internal standards. Any breaches are addressed firmly and

consistently, regardless of seniority, under the Bank’s disciplinary policy.

The high standards of corporate governance continue to be a key priority for the Board. Corporate

governance practices of the Bank are in accordance with the Board-approved Corporate Governance Charter,

Central Bank of Sri Lanka (CBSL) Directions on Corporate Governance, and the Listing Rules of the

Colombo Stock Exchange (CSE) on Corporate Governance. The Bank’s existing corporate governance framework

mandates the responsibilities and duties of the Board and the Management to the shareholders and other

stakeholders towards the promotion of a strong corporate governance culture. The Bank’s corporate

governance framework is well-structured and supported by a strong focus on integrity, accountability,

transparency in the manner of doing business, and clear and timely communication.

Our commitment to strong corporate governance and ethical conduct remains unwavering.

We continually review the framework within which we operate and the processes implemented to ensure

that they reflect the complexities of our business and meet the needs of our stakeholders. The Board

understands the benefits of annual performance evaluations, both for Directors on an individual basis as

well as for the Board as a whole, and looks for ways in which it can improve and develop.

We firmly believe that Board independence is essential to bring objectivity and transparency in the

Management and in the dealings of the Bank. As at the end of the year, the majority of our Board members

– six out of eight – are independent members. An Independent Director functions as the Chairperson of

the Audit, Nomination and Governance, Integrated Risk Management, Human Resources and Remuneration, and

Related Party Transactions Review Committees.

This year too, the Bank achieved a groundbreaking milestone with the issuance of Sri Lanka’s first-ever

Blue Bond, which is listed on the CSE. The listing of Sri Lanka’s first Blue Bond is a significant

milestone for the Bank and for the country. It brought much-needed focus to the development of

sustainable finance and the role it can play in shaping Sri Lanka’s future. We are honoured to have

initiated this effort and confident that it will mark the beginning of a long and meaningful journey in

supporting coastal resilience, clean water, marine restoration, and other essential areas of national

importance.

Building on the successful issuance and dual listing [on the CSE and the Luxembourg Stock Exchange

(LuxSE)] of Sri Lanka’s first ever Green Bond in 2024, we took another bold step by listing the said

bond on the prestigious International Exchanges in GIFT City, India, namely the National Stock Exchange

– International Exchange (NSEIX), and the India International Exchange (IFSC) Limited (India INX). This

multiple listing underscores our commitment to global sustainability standards and expanding access to

international capital markets.

As we look towards the future, community engagement holds a special place in our hearts. We are

committed to expanding our initiatives and social responsibility programmes over the coming year,

contributing positively to the communities we serve.

I confirm to the best of my knowledge that there were no material violations of any of the provisions

of the directions of CBSL, other applicable laws and regulations, codes of conduct, and other related

policies and procedures of the Bank.

J Durairatnam

Chairman

24 February 2026

GRI

2-9

MANDATE OF THE BOARD

The Board is responsible for the Bank’s system of corporate governance, and is committed to maintaining

high standards and developing governance arrangements to comply with best practices. Ultimate

responsibility for the management of the Bank rests with the Board of Directors. The Board focuses

primarily upon strategic and policy issues and is responsible for the Bank’s long-term success. It sets

the Bank’s strategy, oversees the allocation of resources, and monitors the performance of the Bank. It

is also responsible for effective risk assessment and management. The Board has a formal schedule of

matters reserved to it and delegates certain responsibilities to its committees. The Board meetings are

held ordinarily on twelve scheduled occasions during any given year, as well as holding ad hoc meetings

to consider non-routine business, if required.

The interactions in the governance process are shown in the schematic below:

THE BOARD

Responsible for strategy, risk management, succession planning, and policy issues. Sets the tone,

values, and culture of the Bank. Monitors the Bank's progress against the set targets.

CHIEF EXECUTIVE OFFICER

Develops strategy for approval by the Board. Directs, monitors, and maintains the operational

performance of the Bank. Responsible for the application of policies and implementation of

strategy. Accountable for the Bank's performance.

NON-EXECUTIVE DIRECTORS

Exercise a strong independent voice, challenging and supporting the Executive Director.

Scrutinise performance against objectives and monitor financial reporting. Monitor and oversee

risks and controls, determine the Executive Director and Key Management Personnel (KMP)

remuneration, and manage the Board and KMP succession through their committee responsibilities.

CHAIRMAN

Provides leadership and guidance to the Board, promoting high standards of corporate governance.

He is the link between the Executive and Non-Executive Directors.

COMPANY SECRETARY

Advises the Chairman on Governance, together with updates on regulatory and compliance matters.

Supports the Board agenda with clear information flow. Acts as the link between the Board and its

Committees, and between Non-Executive Directors and the Senior Management.

GRI

2-23

2-24

GOVERNANCE FRAMEWORK OF THE BANK

REGULATORY AND INTERNAL POLICY FRAMEWORK

The main elements which encompass the governance framework of the Bank are outlined below:

Directions issued to licensed commercial banks by the Central Bank of

Sri Lanka

Banking Direction No. 05 of 2024 on Corporate Governance issued by the

Central

Bank of Sri Lanka

Companies Act No. 07 of 2007 and amendments thereto

Banking Act No. 30 of 1988 and amendments thereto

Code of Best Practice on Corporate Governance issued by CA Sri Lanka

Internal Elements

Articles of Association of the Bank

Governance Charter

Policy on Related Party Transactions

Code of Conduct of Directors

Employee Code of Conduct

Statement of Policy on Prohibiting Insider Dealings

Policy on Ascertaining Fitness and Propriety

Whistle-blowing Policy

Disclosure Policy

Anti-Bribery and Corruption Policy

Compliance Policy

Financial Consumer Protection Policy

Environmental, Social, and Governance Policy

Investor Relations and Shareholder Communication Policy

Risk Policies

Anti-Money Laundering Policy

Remuneration Policy

Accessibility Policy

Asset Management Policy

Other policies governing operational areas

Directions, Circulars issued by the Securities and Exchange

Commission of

Sri Lanka (SEC)

Acts, Circulars, Gazettes issued by Tax Authorities

Listing Rules of the Colombo Stock Exchange (CSE)

Shop and Office Employees Act No. 19 of 1954 and amendments

thereto

The list of Policies governing Corporate Governance practices of the Bank can be accessed via the link

https://www.dfcc.lk/about-us/governance/company-policies. These policies are reviewed

periodically and changes are introduced as and when required.

The Bank is in full compliance with the requirements of the Policy described in Section 9.5.1 of the

CSE Listing Rules governing matters relating to the Board of Directors.

The Chairman has assigned the CEO to maintain a dialogue with institutional investors and bring any

matters of concern raised by shareholders to the notice of the Board.

Good corporate governance is a mechanism that harmonises the interests of a wide range of stakeholders

of an institution, while contributing to sustainable growth by attracting outside sources of capital.

The Bank practices high standards of corporate governance based on the Organisation for Economic

Co-operation and Development (OECD) principles of good governance.

GRI

2-9

OECD principles of good governance are based on the following six guidelines:

Promoting transparency, being consistent with laws, and clearly articulating division of

responsibilities.

Protecting and facilitating the exercise of shareholder rights, ensuring equitable treatment of all

shareholders and recognising the rights of stakeholders in creating wealth.

Exercising due diligence and responsibility in capital market operations.

Timely and accurate disclosure on all material matters regarding the Bank, including financial

situation, performance, ownership, and governance.

Sustainability and resilience.

By way of an effective Governance Framework, ensuring the strategic guidance of the Bank, effective

monitoring of management of the Board, and the Board’s accountability to the Bank and its

shareholders.

The key corporate governance practices of the Bank are given in this report with specific disclosures

relating to the status of compliance with the mandatory requirements of Direction No. 05 of 2024 of the

CBSL. In addition to the requirements of the CBSL Direction, the corporate governance rules applicable

to listed entities given in Section 9 of the Listing Rules of CSE are also applicable to the Bank. The

Bank is in full compliance with the said CSE Rules on Corporate Governance.

CORPORATE GOVERNANCE STRUCTURE

GRI

2-18

2-19

2-20

GOVERNANCE RELATING TO BOARD REMUNERATION

The Bank follows a structured and transparent process for designing and determining remuneration for

Board and KMPs. Oversight of all remuneration-related matters is entrusted to the Human Resources and

Remuneration Committee and the Committee ensures independence, objectivity, and alignment with best

practices when recommending remuneration structures, contractual terms, and performance-linked pay for

CEO and KMPs. Recommendations made by the Committee are submitted to the Board for approval.

REMUNERATION POLICIES AND PROCEDURES FOR THE BOARD

Remuneration for the Board is governed by a transparent framework designed to uphold accountability,

independence, and regulatory compliance. The shareholders are called upon to pass a resolution at each

Annual General Meeting to authorise the Board of Directors to determine their remuneration. In

determining remuneration, the Board considers benchmarking data from comparable private sector financial

institutions to ensure that the Director fees remain reasonable, appropriate, and competitive.

Non-Executive Directors are remunerated through a fixed monthly retainer and meeting attendance fees,

reflecting their statutory and fiduciary responsibilities. Additionally, fees are paid for participation

in Board Committee meetings, recognising the added oversight responsibilities performed by the members.

Non-Executive Directors are not entitled to any additional benefits for serving on the Board. The

Directors are not eligible to participate in employee share ownership or option schemes, ensuring

independence and avoidance of conflicts of interest.

In line with directions issued by the Central Bank of Sri Lanka (CBSL), the Directors do not receive

retirement benefits, and the introduction of any such benefit would require prior shareholder approval.

This reflects the Bank’s strong adherence to regulatory expectations and governance best practices.

EVALUATION OF BOARD PERFORMANCE

The Board carries out an annual evaluation of the performance, effectiveness, and governance practices

of the Board in accordance with the requirements of the CBSL. The assessment evaluates the collective

performance of the Board against an established set of criteria that reflect regulatory requirements and

best practices. The effectiveness of Board meetings, compliance and regulatory assurance, Committee

reporting, the Board’s adherence to sound governance principles, Board composition, appointments and

succession are covered in the evaluation.

In addition, the Nomination and Governance Committee carries out an annual evaluation of the Board

covering the performance of the Board and how well the Board has carried out its duties during the year,

the evaluation of the Chairman’s role, and the Board’s relationship with the CEO. The assessment also

focuses on the Chairman’s ability to provide leadership to the Board and foster an environment of open

and constructive dialogue, ensure effective participation of all Directors and uphold governance and

ethical standards, manage Board processes, meeting conduct, and information flows efficiently. The CEO’s

annual performance evaluation is carried out by the Board, based on Board-approved goals and

predetermined KPIs. The Human Resource and Remuneration Committee submit recommendations to the Board

regarding performance-linked remuneration and the CEO’s goals for the year.

BOARD CULTURE

The Board of Directors are encouraged to be open and forthright in their approach, with active debate

encouraged during Board meetings before any decisions are taken. We believe this helps to forge strong

and open working relationships, while enabling our Directors to engage fully with the Bank and allowing

them to make their best possible contribution.

BOARD REFRESHMENT

Periodically, the Board welcomes fresh talent due to retirement, resignation, or any other exigency

that prompts the exit of a current Director. Such new appointments infuse new talent and fresh ways of

thinking, which are required for a business that is sustainable.

GRI

2-23

2-24

2-25

2-26

BOARD MEMBERS ACCESS TO INFORMATION

The Directors receive the Board Circulars well ahead the date of the Board Meeting. In addition, they

may request further information or expert advice as they deem necessary to make clear and informed

decisions. On appointment, Directors are provided with an orientation covering the key areas of the

Bank.

CONDUCT AND ETHICAL FRAMEWORK

The Bank’s framework for ethical conduct based on transparency and integrity with strict adherence to

laid down policies and procedures is non-negotiable. This area is governed by several key policies and

procedures.

The Board

The Employees

The Code of Conduct for Directors adopted by the Bank, which the Directors are expected to

abide by, encompasses the following:

Compliance with laws, rules, and regulations

Avoidance of conflicts of interest

Maintenance of confidentiality of information

Fair dealing with stakeholders

Protection of the Bank’s assets

Employee behaviour is governed by a separate Code of Conduct including other policies and

procedures such as the Anti-Bribery and Corruption Policy, Disciplinary Code, Statement of Policy

on Prohibiting Insider Trading, Whistle-blowing Policy, Anti-Money Laundering Policy, Compliance

Policy, Disclosure Policy, etc.

WHISTLE-BLOWING POLICY

This is a vital mechanism for employees to report misconduct, fraud, or unethical practices within the

Bank. The policy establishes a confidential tool for employees to escalate concerns that can potentially

harm the Bank’s reputation or jeopardise the health and safety of employees, without fear of reprisal.

The Bank assures the whistle-blower's confidentiality and pledges to shield them from reprisals.

An investigation will be carried out on any matters brought to notice and, if required, steps will be

taken to rectify the issue.

ANTI-BRIBERY AND CORRUPTION POLICY

The Bank opposes all forms of bribery and corruption. The Anti-Bribery and Corruption Policy governs

the Bank’s Anti-Bribery and Corruption Framework, overseen by the Fraud Risk Management Committee

(FRMC). This process ensures the Bank’s strict compliance with local laws that safeguard its reputation

and standing with the regulators.

The ethos of the policy is applicable to all, including directors, employees, and authorised

representatives, prohibiting engagements with individuals or entities associated with or vulnerable to

bribery and corruption. FRMC conducts routine policy assessments, using audits, compliance checks, and

Human Resource (HR) assessments to ensure alignment with the Bank’s steadfast stance of zero tolerance

towards bribery and corruption. The Employee Code of Conduct also outlines employee conduct guidelines,

including bribery and corruption regulations.

GIFTS AND INDUCEMENTS

Accepting gifts and inducements can compromise objectivity, leading to biased decision-making or

preferential treatment. It undermines trust, potentially damaging the Bank’s reputation and credibility,

and violates ethical standards. Declining gifts and inducements ensures ethical conduct, preserves

professionalism, and upholds the Bank’s integrity, fostering a culture of transparency, fairness, and

trustworthiness.

In terms of the Employee Code of Conduct, employees are prohibited from seeking or receiving gifts and

incentives from customers and other third parties involved in the Bank’s business, except for nominal

token gifts associated with celebratory occasions.

ANTI-MONEY LAUNDERING POLICY

In the current digitised financial landscape where high-value transactions move across accounts and

financial markets, money laundering is an ever-present threat. The Bank’s Anti-Money Laundering Policy

stringently applies the regulatory requirements to ensure it is not used by unscrupulous individuals to

launder money or to utilise funds for illegal purposes.

Staff training is conducted to ensure this is fully ingrained for compliance, and a separate department

is responsible for ensuring the Bank’s policy and procedure stay current with local and global

standards.

GRI

2-9

2-12

2-13

2-14

SUSTAINABILITY, and ENVIRONMENTAL, SOCIAL, AND GOVERNANCE (ESG)

The Board provides strategic oversight to ensure sustainability and ESG considerations are embedded

into the Bank’s business model, operations, short- and medium-term planning, and long-term strategy.

This approach strengthens resilience and supports durable value creation for shareholders and

stakeholders.

Accordingly, sustainability and climate-related matters are built into the Board and Board Integrated

Risk Management Committee agendas, and are evaluated alongside the Bank’s risk appetite, so ESG

oversight is embedded within core governance and risk decision-making rather than treated as a

standalone agenda item.

The Board’s ESG oversight covers:

Strategic Alignment – Integrating sustainability into DFCC Bank's corporate

strategy and capital allocation.

Risk Management – Identifying and mitigating sustainability and climate-related

risks through scenario analysis and stress testing.

Regulatory Compliance – Preparing for SLFRS S1 and S2 disclosures, mandatory

adoption effective from 2025 (transition relief has been obtained where available).

Stakeholder Engagement – Maintaining dialogue with regulators, investors,

customers, employees, and communities to align ESG priorities with stakeholder expectations.

Innovation for Sustainable Finance – Driving green finance (both lending and

fundraising), renewable energy lending, and inclusive banking solutions.

The Bank integrates ESG risks and opportunities into strategic and business plans presenting the Board

with short-medium-and long-term ESG targets linked to DFCC Bank's Sustainability roadmap.

THE GOVERNANCE FRAMEWORK FOR SUSTAINABILITY AND ESG

To strengthen ESG integration across its operations, the Bank has established a multi-tier governance

structure. At Board level, the Board Integrated Risk Management Committee (BIRMC) provides dedicated

oversight on sustainability-related risks and opportunities, ensuring ESG considerations are embedded

into the Bank’s risk governance framework and strategic decision-making. BIRMC, comprising three Board

representatives along with the CEO and the Deputy Chief Executive Officer (DCEO), is supported by Key

Management Personnel including the Chief Risk Officer, Chief Compliance Officer, Head of Treasury, and

Head of Sustainability as permanent invitees. This structure also aligns with SLFRS S1, which requires

clear governance for sustainability disclosures. The Executive Sustainability Management Committee

(ESMC) chaired by the CEO is the executive level management committee that provides management level

oversight on sustainability governance. Complementing this, the Sustainability Management Committee

(SMC) operates as a second-tier management committee under ESMC. Chaired by the DCEO, SMC acts as a

working group to monitor ESG performance, review progress against targets, and drive strategic

priorities through cross-functional collaboration with representatives from key departments and business

units. Together, these committees ensure that ESG principles are integrated into DFCC Bank's

strategy, operations, and reporting, reinforcing the Bank’s commitment to responsible and sustainable

banking.

Terms of Reference of ESMC and BIRMC were updated during the year to reinforce sustainability-related

financial disclosures and clarify roles for successful ESG implementation. Importantly, every employee

plays a vital role in contributing to the Bank’s sustainability strategy, ensuring that sustainability

is embedded across all levels of the organisation. Through this collective effort and strong governance,

the Bank continues to drive resilience, innovation, and long-term stakeholder value.

ENHANCING ESG CREDENTIALS THROUGH ESMS IMPLEMENTATION

The Board remains firmly committed to strengthening the Bank’s ESG credentials as a strategic priority.

To this end, the Bank has implemented a robust Environmental and Social Management System (ESMS) since

2016 to identify, assess, and mitigate environmental and social risks within credit operations, thereby

reducing its environmental footprint and enhancing social impact. Governance has been reinforced through

the Management Credit Committee and the appointment of a dedicated ESMS Officer to oversee the

integration of environmental and social risk considerations across all operations. Complementing this,

the Bank has formalised its approach through the ESG Policy, while fostering employee engagement via

regular training programmes. Capacity-building initiatives on environmental and social due diligence are

conducted regularly by the Sustainability Department in collaboration with the Learning Academy,

ensuring staff are equipped to uphold the Bank’s sustainability objectives.

GRI

2-17

BOARD CAPACITY BUILDING ON SUSTAINABILITY AND ESG

The Bank recognises that effective oversight of sustainability matters requires a well-informed and

capable Board. To strengthen governance capability, the Bank invests in continuous training and

knowledge enhancement for Board members and senior management on critical sustainability topics,

including ESG principles, climate-related risks, SLFRS S1 and S2 disclosure requirements, and global

sustainability trends.

During the year, the Board actively participated in ESG and sustainability-related training, awareness

programmes, and knowledge-sharing sessions organised by the Bank and leading external experts. These

initiatives ensure that the Board collectively builds expertise, remains informed of emerging ESG

developments, and reinforces its role in guiding DFCC Bank's sustainability strategy.

Programme description

Attendance

Sustainability reporting and the Implementation of SLFRS S1 and S2:The session

included: Evolution of ESG/sustainability, an introduction to slfrs sustainability disclosure

standards, adoption of SLFRS sustainability disclosure standards, governance-related disclosure

requirements.

09

Awareness session on Cybersecurity:The session included: Understanding

Information security and privacy, current threat landscape in the finance sector, case studies of

security breaches, strategies for enhancing security and privacy, role of the Board in Information

security governance.

09

McKinsey Turbo charging growth through AI: The programme included an overview

of Artificial Intelligence (AI) and its impact in financial services.

09

Awareness session on Companies (Amendment) Act No. 12 of 2025, Amendments to the CSE Listing

Rules and Directors Relevant Interest.

09

Workshop on “Can Banks De-Risk and Innovate in this Hyper-Competitive Age with Technology.”

02

Workshop on Board’s Role in Mandatory Sustainability Reporting.

02

Improving the Governance Framework: Ensuring greater accountability of the

Board of Directors for the compliance obligations of Anti-Money Laundering, Countering the

Financing of Terrorism, and Proliferation Financing.

02

In addition, the Bank circulated an awareness questionnaire on SLFRS S1 and S2 and a training needs

assessment focused on sustainability-related financial disclosures for the Board ensuring strong

engagement in preparing for the upcoming regulatory requirements.

INTEGRATED REPORTING

The Bank places a strong emphasis on integrated reporting, combining financial and non-financial

information to provide a transparent and holistic view of the Bank’s performance. This approach enhances

accountability and meets the growing expectations of stakeholders for responsible and ethical business

practices.

The Board has taken deliberate steps to evaluate ESG risks and opportunities and embed these

considerations into the Bank’s operations and strategic planning. By integrating sustainability into

decision-making, DFCC Bank fosters resilience, supports long-term growth, and strengthens its ability to

manage emerging risks effectively.

To ensure informed decision-making, the Board is updated on sustainability performance on a quarterly

basis through the BIRMC and may, from time to time, request comprehensive analysis reports from internal

teams and external experts to maintain adequate due diligence. Additionally, the Board reviews ESG

factors as necessary to strengthen and enhance ESG-related areas within the Bank’s operations.

Upholding the highest standards of corporate governance, the Board ensures that our actions contribute

to long-term value creation, robust risk mitigation, and sustainable development. This comprehensive

approach underscores the Bank’s unwavering commitment to responsible banking and sustainability

leadership.

Further details on the Bank’s sustainability framework and initiatives are presented in the following

sections of this Annual Report:

The Board is also responsible for ensuring that management maintains a system of internal control that

provides assurance of effective and efficient operations, internal financial controls, and compliance

with laws and regulations. In carrying out this responsibility, the Board gives due consideration to

what is appropriate for the Bank’s business and reputation, the materiality of financial, and the

relative costs and benefits of implementing specific controls. The Board is also the decision-making

body for all other matters of importance to the Bank as a whole due to their strategic, financial, or

reputational implications or consequences. There is a formal schedule of matters reserved for the

Board’s decision. Our risk management process identifies the key risks facing each business and reports

to the Board on how those risks are being managed. Such a system of internal control can only be

designed to manage, rather than eliminate, risk of failure, to achieve business objectives, and can

provide reasonable but not absolute assurance against material misstatement and loss. The Board has a

process for identifying, evaluating, and managing the risks we face. That process is continual and has

been in place for the year under review up to and including the date of this report.

Further aspects that impact the internal control framework of the Bank are covered under Integrated

Risk Management on pages 239 to 267.

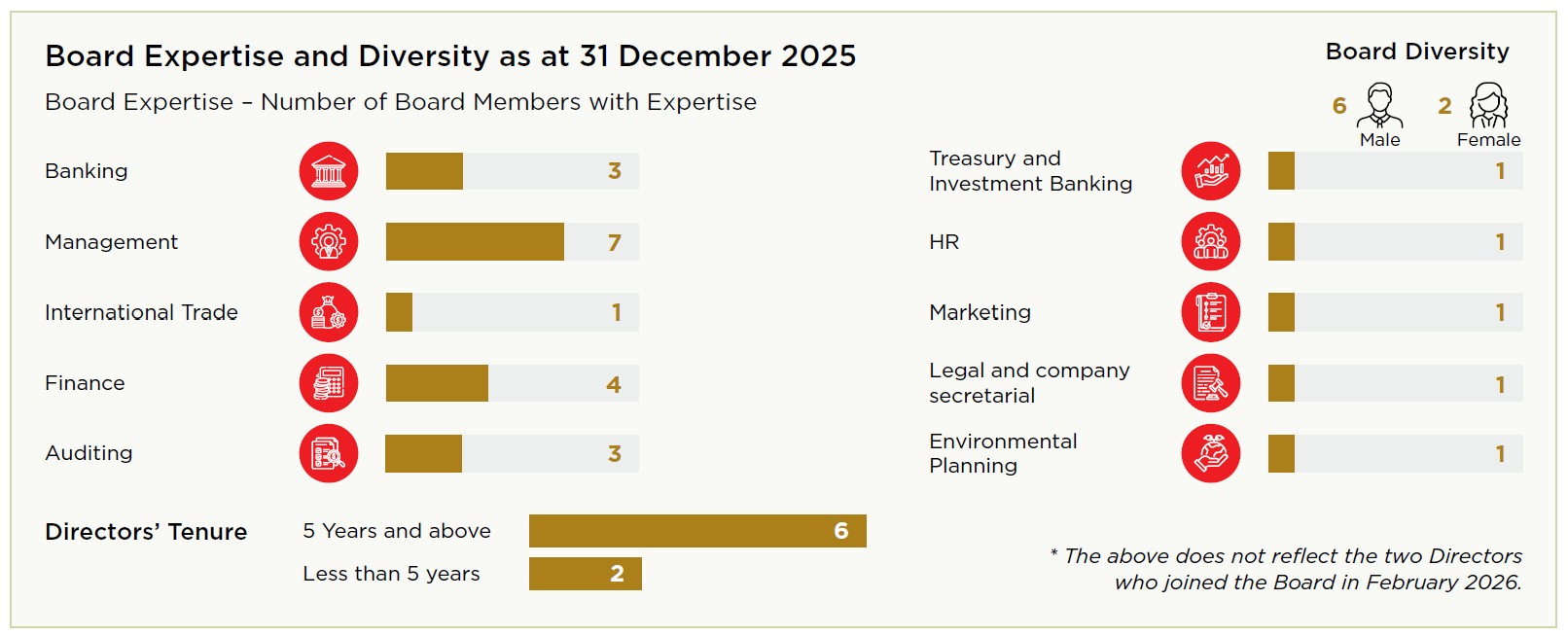

Board Expertise and Diversity

The Board brings together a well-balanced blend of professional expertise, industry knowledge, and

diverse perspectives essential for guiding the Bank’s strategic direction and governance

responsibilities. This spectrum of competencies ensures that the Board is equipped to provide robust

oversight, informed decisions, and effective stewardship in driving the Bank’s long-term value creation

and sustainable growth.

BOARD OF DIRECTORS

The Directors of the Bank as at 31 December 2025 categorised in accordance with the criteria specified

in the Banking Act Direction No. 05 of 2024 issued by the CBSL are as follows:

Independent Non-Executive Directors

J Durairatnam – Chairman

Ms L K A H Fernando

N K G K Nemmawatta

Ms A L Thambiayah

N Vasantha Kumar

H A J de S Wijeyeratne

Non-Independent Non-Executive Director

P A Jayatunga

Executive Director

N H T I Perera – Chief Executive Officer

The Independent Directors satisfy the criteria set out in section 9.8.3 of the CSE Listing Rules.

Further, all Directors satisfy the fit and proper assessment criteria stipulated in the CSE Listing

Rules.

None of the above Directors (including close family members) has had any relationship with the other

Directors.

GRI

2-12

2-23

2-24

BOARD HIGHLIGHTS 2025

Approved the Strategic Plan for 2025-2029

Revised the limits on delegation of authority on lending and related activities

Revised the limits on delegation of authority for capital and revenue expenditure

Decided to carry out a brand health/equity study for the Bank

Approved the payment of a dividend of LKR 6 per share (scrip and cash) for 2024

Approved the Accessibility Policy

Approved the Policy on Financial Consumer Protection

Approved the appointment of two new Directors to the Board subject to the approval of CBSL

Approved the listing of DFCC Bank's Green Bond on the National Stock Exchange International

Exchange (NSEIX) India and on the India International Exchange (IFSC) Limited (India INX)

Approved the establishment of a fully owned subsidiary to focus on value added financial services

including wealth management, underwriting, and corporate financial advisory to clients

Approved the implementation of a Programme for Service Excellence

Approved the Sustainable Bond Framework

Conducted awareness sessions for Directors on:

– Cybersecurity and Amendments to the Companies Act

– The Board’s Role in Sustainability Reporting and the Implementation of SLFRS S1 and S2

Decided to issue up to 100,000,000 Basel III Compliant, Subordinated, Listed, Rated, Unsecured,

Redeemable GSS+ Bonds

Decided to issue up to 30,000,000 Senior, Listed, Rated, Unsecured, Redeemable Blue Bonds

Approved the Corporate Social Responsibility (CSR) Project on Leopard Conservation

Decided to enter into an agreement with Standard Chartered Bank for the acquisition of their wealth

and retail banking business in Sri Lanka

Revised the Terms of Reference of Board Committees

Reviewed all major policies

Reviewed and endorsed the Key Performance Indicators (KPIs) of Key Management Personnel

PERMANENT BOARD COMMITTEES AS AT 31 DECEMBER 2025

*The Credit Restructure Committee approves papers by circulation

Attendance of Directors at meetings – 2025

Name of Director

Main

Board

Audit

Committee

Human

Resources and

Remuneration

Committee

Nomination and

Governance

Committee

Integrated

Risk

Management

Committee

Credit

Approval

Committee

Related Party

Transactions

Review

Committee

Total number of meetings

14

10

2

7

6

12

12

J Durairatnam

14/14

1/1

2/2

7/7

12/12

12/12

Ms L K A H Fernando

14/14

10/10

W R H Fernando

13/14

8/9

7/7

6/6

P A Jayatunga

14/14

2/2

6/6

N K G K Nemmawatta

14/14

12/12

12/12

N H T I Perera

14/14

Ms A L Thambiayah

11/14

2/2

11/12

11/12

N Vasantha Kumar

13/14

7/7

6/6

H A J de S Wijeyeratne

14/14

10/10

Attended/eligible to attend

SHAREHOLDER RIGHTS

The basic rights of shareholders include;

The ability to transfer shares freely

To have access to financial and other relevant information about the entity on a regular and timely

basis

The ability to effectively participate in shareholder meetings

Appoint Directors and Auditors

Equitable treatment relating to the type of shares owned.

The shares of the Bank are freely transferable through the Colombo Stock Exchange (CSE) but subject to

limitations stated in the Articles of Association of the Bank and the Banking Act.

The Board approved Investor Relations and Shareholder Communication Policy ensures that information

relating to the financial performance and progress of the Bank is made available to shareholders through

timely disclosures made to the CSE.

During the year, shareholders were notified, through announcements made to CSE, of quarterly results,

dividend declaration for 2024, Annual Financial Statements for 2024, Interim Financial Statements for

2025, date of the Annual General Meeting in 2025, date of the Extraordinary General Meeting in 2025,

GSS+ Bond Issue, Blue Bond Issue, etc. The Bank’s website has a dedicated area “Investor” for investors,

which includes Interim Financial Statements, Annual Reports, and Debt Instruments.

The Annual Report contains a comprehensive review of performance as well as other information of

relevance to the other stakeholders apart from reporting on the financial condition of the Bank and the

Group. All important information is given publicity through the print and electronic media and posted on

the Bank’s website.

The Bank has procedures to promptly disseminate price-sensitive information and trading in shares by

the Directors to the CSE, as required by the Listing Rules. In instances where this is not possible, the

Chief Financial Officer advises closed periods for trading in the Bank’s shares by employees and

Directors. The Board has formally adopted a Statement of Policy Prohibiting Insider Trading. As a

general rule, the period after the end of each quarter up until two market days after the financial

information is released is treated as closed periods. Procedures are in place to detect any violations.

During the year under review, the Bank shared a reasonable portion of its profit for 2024 with

shareholders in the form of cash dividend, while retaining the balance funds to support its growth and

development. This year, the Bank also distributed part of the dividend as a scrip dividend.

All shareholders of the Bank are treated equally on the basis of one vote per ordinary share. The Bank

has not issued any non-voting ordinary shares or preference shares.

SHAREHOLDER MEETINGS

The Annual General Meeting (AGM) of the Bank is normally held within a period of one year from the date

of the previous meeting, after giving adequate notice to shareholders as required by the Articles of

Association. Accordingly, the AGM was held on 28 March 2025.

The Annual Report and Notice of Meeting are sent to all shareholders in order to enable effective

shareholder participation at the meeting. The shareholders have the opportunity to access the Annual

Report via a web link or obtain a printed document.

Extraordinary General Meetings (EGM) are held to obtain shareholder approval on matters that require

such approval. An EGM was held on 30 October 2025 to obtain the approval of shareholders for the GSS+

Bond issue.

Annual Corporate Governance Report for the year Ended 31 December 2025 Published in Terms of Section

1.11 of the Banking Act Direction No. 05 of 2024

Section

Governance principle

Compliance

Remarks

1.

Ultimate Responsibility and Accountability of the Board

Compliant

The Board is ultimately responsible and accountable for overseeing the Bank’s affairs,

governance framework, business strategy, financial soundness, and risk management, and for

ensuring compliance with all applicable laws, regulations, and sound banking practices.

Directors make objective decisions in the best interests of all stakeholders. Board decisions

are taken collectively and duly recorded, with any dissent by a Director expressly noted in the

minutes.

1.1

Responsibilities of the Board

Compliant

The Board has strengthened the safety and soundness of the Bank through the implementation of

(a) to (w) as given below.

(a) Strategic objectives and corporate values

Compliant

The Bank sets its strategic objectives and goals for the long-term through the functional

strategic plan which is approved by the Board. These goals and the corporate values approved by

the Board are communicated to the business units and other staff. The corporate values are

posted on the Bank’s intranet and all employees are guided by these values.

(b) Overall business strategy

Compliant

The Bank’s Strategic Plan was approved by the Board in January 2025. It was formulated

covering the period 2025-2029, with a higher level of emphasis on the period 2025-2027, with

indicative objectives for the remaining period.

The Board engages in the strategic planning and control of the Bank by overseeing the

formulation of business objectives and targets, assessing risks by engaging qualified and

experienced personnel, delegating them with the authority for conducting operational activities

and monitoring performance through a formal reporting process.

A separate item has been included in the agenda at every Board meeting under the heading

“Strategic Discussion” to take up any matter of strategic importance to the Bank. Directors are

encouraged to identify and communicate any matter they consider to be of strategic importance.

Periodic updates or revisions of the Strategic Plan are considered and formulated as and when

needed.

(c) (i) Identify principal risks and ensuring implementation of appropriate systems to

manage risk.

Compliant

Integrated Risk Management Framework was reviewed during the year.

The Board Integrated Risk Management Committee (BIRMC) appointed by the Board has Bank-wide risk

management oversight and assists the Board in fulfilling its statutory responsibilities. The

BIRMC's primary function is to assist the Board in fulfilling its risk management

responsibilities as required by business needs, internal policy guidelines, and applicable laws

and regulations.

(c) (ii) Establish well-defined organisational responsibilities for the three lines of

defence

Compliant

In the governance structure, management control at the business level and relevant internal

control mechanisms act as the first line of defence, where they are responsible for the

strategy, performance, and risk management of the Bank.

The Bank has centralised oversight of effective implementation of risk management framework as

the second line of defence, which is responsible for the policy implementation, monitoring, and

oversight. This is mainly done by Integrated Risk Management Department and Compliance

Department.

The Internal Audit function acts as the third line of defence, which provides the organisation

with independent and objective assurance on the risk exposures, processes, and practices in

place.

(c) (iii) Ensure that the risk management, compliance, and internal audit functions are

positioned and resourced to carry out the responsibilities

Compliant

The Board ensures that the Risk Management, Compliance, and Internal Audit functions are

appropriately structured, sufficiently staffed, and adequately resourced to operate

independently and effectively. The Board approves their mandates, reviews their performance on a

regular basis, and provides the necessary authority and resources to discharge their

responsibilities in line with regulatory requirements and best practices.

(c) (iv) Define the risk appetite of the Bank aligning with strategic, capital, and financial

plans

Compliant

The Bank has an internally developed Risk Appetite Statement, which was approved by the Board

and it is reviewed periodically. The Risk Appetite Statement is aligned with the Bank’s

strategic objectives, capital planning, and financial plans.

(c) (v) Outline the actions to be taken when stated risk appetite limits are breached.

Compliant

The Bank continuously monitors the risk limits based on the Risk Appetite Statement and

actions are taken when risk limits are near breach or breached. Overall Risk Limits are

periodically submitted to the relevant Management Committee, BIRMC, and the Board highlighting

near breaches and breaches.

(d) Avoidance of Board dominance

Compliant

The Board-approved Policy on Directors Code of Conduct ensures that the Board is not

dominated or significantly influenced by a Director or a group of Directors in a manner

detrimental to the interest of the Bank as a whole.

(e) Communication with stakeholders

Compliant

The Board-approved Investor Relations and Shareholder Communication Policy ensures that

information is made available to shareholders and other stakeholders through timely disclosures

made to the Colombo Stock Exchange (CSE), and by publicity through the press and electronic

media and posts on the Bank’s website.

The Bank has an internally developed Code of Conduct for its employees, which is posted on the

Bank’s intranet and is accessible by all employees. The Bank has also adopted a separate Code of

Conduct for the Directors.

(f) Bank’s internal control and management information systems

Compliant

The Audit Committee assists the Board in reviewing and evaluating the integrity, adequacy,

and effectiveness of the internal control system, including management information systems and

controls over the financial reporting of the Bank.

The Internal Audit carried out quarterly reviews to ensure that the internal control systems are

functioning as appropriate.

The report by the Board of Directors on Internal Control over Financial Reporting is given on

page 288. The Independent Assurance Report by the External Auditor on the Directors’ Statement

on Internal Control is given on page 291.

(g) Managing related party exposures

Compliant

The Related Party Transaction Review Policy is in place to ensure that related party

transactions are managed in such a way to avoid conflict of interest. Further, the related party

transactions are reviewed by the Related Party Transactions Review Committee.

(h) Business continuity and disaster recovery plans

Compliant

The Bank has a comprehensive Business Continuity Plan (BCP) and a Disaster Recovery (DR)

covering all critical functions and systems to ensure financial stability, operational

resilience, and preserve critical operations during any disruptive event. The Bank has obtained

ISO 22301 certification for Business Continuity Management Systems (BCMS).

(i) Oversee the approach to remuneration

Compliant

The Board oversees the Bank’s approach to remuneration through the Human Resources and

Remuneration Committee, which reviews and recommends all increments and changes to the

remuneration of the CEO and Key Management Personnel (KMP) for Board approval.

The Committee also reviews and recommends changes to benefit schemes, ensuring that remuneration

practices are aligned with the Bank’s risk culture, risk appetite, and long-term strategic

objectives.

(j) Key Management Personnel (KMP)

Compliant

The Board has identified and designated its Key Management Personnel.

(k) Authority and responsibility of the CEO and KMP

Compliant

Areas of authority and key responsibilities of Directors have been set out in the Corporate

Governance Charter which has been adopted by the Board. The Board has also identified matters

specifically reserved for the Board. The duties and responsibilities of other KMP are formally

documented in their job descriptions. Delegation of authority levels for KMP has also been

clearly specified in Board-approved circulars.

(l) Oversight of the affairs of the Bank by the CEO and KMP

Compliant

Oversight is exercised through Board Committees, reporting to the Board as appropriate.

Policies and decisions of the Board requiring appropriate follow up are communicated by the

Board Secretary to the relevant KMP.

Minutes of relevant management committee meetings headed by the Chief Executive Officer (CEO)

are submitted to the Board for information. KMP are called upon to clarify matters and make

presentations on matters within their purview at the monthly Board meetings.

(m) Board’s own governance practices

Compliant

An annual self-assessment is carried out on a structured format where the Directors submit

their individual responses directly to the Board Secretary. The responses are collated by the

Board Secretary and submitted to the Board. The effectiveness of the Board’s own governance

practices is reviewed by the Board and areas for improvement are discussed for necessary action.

During this year too, in addition to the assessments carried out by the individual members, the

Nomination and Governance Committee, based on a separate checklist, carried out an evaluation of

the Board and the results were shared with the other members of the Board and an opportunity was

provided to them to comment on the findings of the Committee.

(n) Self-assessment of the Board of Directors

Compliant

The Board has a structured scheme of self-assessment which is carried out annually. The

performance of the respective committees is also evaluated by the other members who are not

members of the respective committees, in order to ensure that they function effectively. The

findings are discussed at the Board meetings and action is taken on areas identified for

improvement.

The performance assessment criteria of the CEO is given in 5.4 a).

(o) Succession plan for the CEO and the KMP

Compliant

The Bank has in place a succession plan for the CEO and the KMP, which is reviewed annually

by the Nomination and Governance Committee and approved by the Board.

(p) Regular meetings with CEO and KMP to monitor progress

Compliant

Meetings are attended by relevant executives when required. Additional information sought by

Directors on papers submitted to the Board is clarified by the respective officers. The Board

has free access to Senior Management.

During the year, the Board reviewed the performance in order to monitor progress against the

budget. This provided an opportunity for the Board members to interact with the Senior

Management to clarify reasons for variations against budget and to suggest corrective action.

(q) Regulatory environment

Compliant

The Board Secretary/Compliance Officer provides all regulatory information required to the

Board members. The Compliance Officer submits monthly and quarterly compliance reports to the

Board.

The CEO briefs the Board on specific issues. Senior Management maintains continuous dialogue

with the Regulator to ensure an effective relationship.

During the year, the Board was apprised of the changes introduced by the Companies (Amendment)

Act No. 12 of 2025 and the amendments to the CSE Listing Rules.

(r) Due diligence in hiring and oversight of External Auditor

Compliant

The primary responsibility for making recommendations on the appointment of the External

Auditor rests with the Audit Committee. A formal policy approved by the Board on engagement of

the External Auditor to perform non-audit services is in place.

(s) Professional and ethical conduct

Compliant

The Bank has adopted a separate Code of Conduct for the Directors, to ensure professional and

ethical behaviour, and that no undue benefits are received by them.

(t) Sound corporate culture

Compliant

The Bank has an internally developed a Code of Conduct both for its Directors and employees.

The corporate values approved by the Board are also accessible by all employees.

(u) Rectification of supervisory concerns

Compliant

A quarterly update on the supervisory concerns is reviewed by the CEO to ensure rectification

prior to submission to the Regulator.

(v) Whistle-blowing Policy

Compliant

The Board has adopted a Whistle-blowing Policy to encourage employees to communicate

legitimate concerns on any illegal or unethical practices. The policy is reviewed on an annual

basis.

The policy clearly states the persons to whom the concerns can be escalated within the Bank,

procedures for investigating legitimate material concerns raised by the employees, procedures to

ensure protection and anonymity of the employees who raise concerns due to any detrimental

treatment or reprisals, and alternative avenues for whistle-blowing to regulators.

Arrangements are in place for fair and independent investigation and follow-up action.

(w) Promote sustainability

Compliant

The Bank has treated sustainability as a core pillar of its business strategy. As the

country’s pioneering lender for sustainability initiatives, the Bank has a well-articulated

sustainability strategy in place.

The Board, through the BIRMC, has the overall governance over the sustainability activities of

the Bank, which are carried out under the guidance and monitoring of the Executive

Sustainability Management Committee (ESMC), led by the CEO. The Bank reports the progress of its

sustainable lending activities to the CBSL on a quarterly basis in compliance with the Sri Lanka

Green Finance Taxonomy and Banking Act Direction No. 05 of 2022.

The Sustainability Strategy and the Environment, Social and Governance (ESG) Policy of the Bank

are reviewed periodically. The Bank has a Sustainable Bond Framework (which is used for raising

funds by the Bank using Green, Blue and Sustainable bonds), which has been prepared in line with

ICMA principles on sustainable bonds, with a limited assurance by an independent assurance

provider (KPMG).

In addition, the Board is periodically apprised of the status, activities, and progress of the

sustainability activities of the Bank.

1.2

Appointing Chairperson and CEO

Compliant

The Board elects the Chairman and appoints the CEO. While the Chairman provides leadership to

the direction, oversight, and control process exercised by the Board, the CEO is responsible for

the management of the Bank.

1.3

Board Meetings

Compliant

The Board held 14 meetings during the year. The Directors actively participated in the

Board’s decision-making process. Seeking approval of the Board by circulation was done only in

exceptional circumstances due to urgency, and such approvals are ratified at the Board meeting

held immediately following the circulation.

1.4

Board Procedures

(a) The Board to ensure that arrangements are in place for Directors to include items and

proposals in the agenda of Board meetings

Compliant

Whenever the Directors suggest topics for consideration at the Board meetings, they are

included in the agenda under “open discussion”, which is an integral part of every Board

meeting, and other supporting data, reports, documents, etc., relevant for the subject matter

are circulated among the Directors for information.

(b) Notice of Board meetings – at least seven days’ notice of regular meetings and

reasonable notice of other meetings to be given

Compliant

Dates for regular monthly Board meetings are agreed by the Directors at the start of each

year, and any changes to dates of scheduled meetings are decided well in advance. The Board

Circulars and other documents pertaining to meetings are made available well in advance to

enable all Directors to participate in deliberations.

(c) Attendance at Board meetings

Compliant

All Directors attended more than two-thirds of Board meetings and no Director was absent for

three or more consecutive meetings. Attendance details are given on page 215.

1.5

Appointing a Company Secretary

(a) Duties and qualifications of the Company Secretary

Compliant

The Company Secretary possesses the qualifications specified in Section 43 of the Banking

Act.

The Company Secretary, while performing the secretariat services to the Board and shareholders’

meetings, is responsible to the Board in ensuring that Board procedures and applicable rules and

regulations are followed.

All new Directors are provided with the necessary documentation on Directors’ responsibilities

and specific banking-related directions/policies that are required to perform their function

effectively.

(b) The Directors’ access to the Company Secretary

Compliant

All Directors have access to the advice and services of the Company Secretary directly.

(c) Implementation of the recommendations by the Nomination and Governance Committee on

training

Compliant

The Nomination and Governance Committee recommends training and capacity-building programmes

for Directors, and the Company Secretary ensures the timely implementation by coordinating and

organising relevant training and awareness programmes approved by the Board.

(d) The Company Secretary’s duty to maintain minutes of Board meetings together with

recordings and ensure availability for the Directors’/Regulator inspection

Compliant

The Company Secretary compiles the minutes of the Board meetings, which are subject to

approval of the Board and signed by the Chairman and the Secretary. Copies of minutes are

provided and Directors/Regulator have access to the original minutes/recordings at reasonable

times.

1.6

Maintenance of Board Meeting Minutes – the form and contents of the minutes of Board meetings

Compliant

The Board minutes are drawn with reference to Board Circulars with sufficient details to

indicate the decisions made by the Board. The information used in making such decisions, the

reasons and rationale of making them and each Director’s contribution if considered material, is

included in the minutes.

GRI

2-15

Section

Governance principle

Compliance

Remarks

1.7

Independent Professional Advice on request for Directors to perform their duties

Compliant

The Board has put in place a procedure where the Directors can obtain independent

professional advice, at the Bank’s expense, to perform their duties.

1.8

Managing Conflicts of Interest

(a) The Directors’ avoidance of conflicts of interest

Compliant

The Companies Act No. 07 of 2007 requires Directors who are directly or indirectly interested

in contracts or a proposed contract with the Bank to declare the nature of such interest. The

Directors have declared their interests in contracts involving the Bank.

(b) The Directors shall abstain from participating in the decision and not receive

information relating to it where there is an interest

Compliant

A separate agenda item has been created for matters where Directors have an interest, and

those who have an interest do not participate in such decisions and have no access to

information relating thereto.

(c) Relationship among the Directors, CEO, and KMP

Compliant

The relationship between the Directors themselves and between the Directors, CEO, and KMP are

maintained at a level that does not result in undue influence.

(d) Policy on identifying and managing conflicts of interest

Compliant

The Board-approved Policy on Directors Code of Conduct ensures identification and managing

conflicts of interest. The policy also specifies measures to be taken in the event of

non-compliance.

1.9

Requirement to inform inability to meet obligations

Compliant

Solvency is a matter constantly monitored by the Treasury Department, BIRMC, and the Board.

During the year under review, the Bank remained solvent and no event has or is likely to occur

that would make the Bank unable to meet its obligations.

1.10

Compliance with Prudential Requirements

Compliant

The Bank is capitalised above the minimum levels required by the Governing Board in terms of

the capital adequacy and minimum required capital.

1.11

Annual Corporate Governance Report

Compliant

The Annual Corporate Governance Report forms an integral part of the Bank’s Annual Report.

2.

Board’s Composition

Compliant

The Board’s composition ensures a healthy mix of knowledge, qualifications, skills,

experience in relevant disciplines, and gender, and they have varied backgrounds to promote

diversity of views commensurate with the size, scale, diversity, and complexity of operations of

the Bank.

2.1

Procedure for Appointing Directors

(a) Appointments of new Directors

Compliant

Appointments of new Directors are formally evaluated by the Nomination and Governance

Committee and recommended to the Board for approval.

The appointment of two new Directors was approved by the Board during the year, subject to

obtaining the approval of the CBSL.

(b) Appointment of a Director or an employee to another bank

Compliant

No Director or employee of the Bank is a Director of another bank.

(c) Directors representing shareholders that have acquired voting rights in contravention

of Banking Act/Directions

Compliant

No such situation has arisen.

2.2

Number of Directors

(a) Number of Directors

Compliant

During 2025, the Board comprised a minimum of eight and a maximum of nine Directors.

(b) Female representation

Compliant

During 2025, the Board consisted of two female representatives.

2.3

Executive Directors

Compliant

The CEO is the only Executive Director on the Board.

2.4

The knowledge skills, experience, and track records of Non-Executive Directors

Compliant

Non-Executive Directors possess strong professional backgrounds, integrity, and high-level

managerial experience in banking, business, industry, law, finance, auditing, etc., enabling

them to exercise independent judgment and contribute effectively to the long-term sustainability

of the Bank.

2.5

Independent Directors

(a) Number of Independent Directors

Compliant

There were six Independent Directors on the Board at the end of the year, which is over half

of total number of Directors.

The Board has adopted a format of a declaration to be obtained quarterly from Non-Executive

Directors, so that each Director shall independently confirm their status against specific

criteria applicable to the ascertainment of independence. As such, all Non-Executive Directors

have submitted their declaration in compliance with the Board decision.

(b) Criteria for Independence

Compliant

All Independent Directors satisfy the criteria set out in 2.5 (b).

(c) Disclosure of details of Directors

Compliant

The names and the composition of the Directors by category are disclosed in the Corporate

Governance Report.

2.6

Representation through Alternate Directors

(a) Maximum period of Alternate Director

Not Applicable

No Alternate Directors were appointed during 2025.

(b) Alternate Directors to represent Independent Directors

Not Applicable

(c) Appointment of an Alternate Director

Not Applicable

(d) Same individual not be appointed as Alternate for two Directors

Not Applicable

2.7

Quorum for the Board Meetings

Compliant

The Bank has been compliant with this rule at all times, as monitored by the Company

Secretary.

GRI

2-25

Section

Governance principle

Compliance

Remarks

3.

Suitability of Directors

3.1

Criteria to Assess Fitness and Propriety

Compliant

The Directors have met the criteria for assessing fit and propriety as provided in the

Banking Act.

3.2

Additional Requirements for Suitability of Directors

(a) Maximum age of Directors

Compliant

All Directors are less than 70 years of age.

(b) Period of service of a Director

Compliant

No Director has held the position of a Director of the Bank for more than nine years.

(c) Not holding Director positions in more than 20 companies/entities

Compliant

All Directors comply with this requirement.

(d) Sufficient time to carry out the responsibilities

Compliant

All Directors comply with this requirement.

3.3

Cooling-off Period

Appointment of a Director or a CEO who has held office in another licensed commercial bank, not

to be considered before the expiry of a period of 6 months from the date of cessation of his/her

office at the licensed bank in Sri Lanka

Compliant

The Company Secretary ensures that all newly appointed Directors comply with this

requirement.

4.

Delegation of Functions

4.1

Division of Responsibilities

Compliant

There is a clear division of responsibility at the Board level and the key management level

to ensure balance of power and authority.

4.2

Specific Matters for Board Decisions

Compliant

Schedule of matters reserved for the Board has been decided on.

4.3

Restrictions to Delegate

Compliant

The delegation of authority made by the Board is designed to facilitate efficient management

of the affairs of the Bank and to aid the oversight role exercised by the Board, it is not of an

extent to hinder the ability of the Board to discharge its functions. The Board retains the

authority to expand, curtail, limit, or revoke such delegated authority.

4.4

Review of Delegation Process

Compliant

The delegation process is subject to periodic review by the Board, to ensure that necessary

amendments are approved to meet the requirements of the Bank. Material decisions made under

delegated authority are reported to the Bank for information.

5.

The Chairperson and CEO

5.1

Division of Responsibility between Chairperson and CEO

Compliant

The Chairman and the CEO are two separate individuals, and the responsibilities of the

Chairman and CEO are set out in writing.

5.2

Suitability of the Chairperson

(a) The Chairperson to be an Independent Non-Executive Director

Compliant

The Chairperson is an Independent Non-Executive Director.

(b) If a Non-Independent Director is serving as the Chairman, such Director may continue

not beyond 31 December 2027

Not Applicable

The Chairman is an Independent Director.

(c) A Chairperson appointed after the effective date to be an Independent Non-Executive

Director

Not Applicable

5.3

Responsibility of the Chairperson

(a) Provide leadership to the Board

Compliant

The Chairman provides leadership to the Board and ensures that the Board discharges its

responsibilities effectively.

(b) Key issues to be discussed at the Board

Compliant

The Chairman encourages members to actively participate and to raise their independent

judgement on all key and appropriate issues in a timely manner.

(c) Agenda of Board meetings

Compliant

The agenda of each Board meeting is drawn by the Company Secretary under the direction of the

CEO and the Chairman, and any matters relevant to the policies and operations of the Bank

proposed by other Directors are included in the agenda upon approval by the Chairman.

(d) Providing information to the Directors

Compliant

The Chairman ensures that all Directors are properly briefed on issues which arise at Board

meetings and ensures that they receive adequate information in a timely manner.

The agenda and all Board papers are circulated electronically to Board members prior to the

meeting.

(e) The Board to act in the best interest of the Bank

Compliant

The Chairman encourages exercise of independent judgement by the Directors on matters under

consideration by the Board in order for the best interests of the Bank to be assured.

(f) Effective contribution of Non-Executive Directors

Compliant

The Chairman facilitates contributions by the Non-Executive Directors in making decisions.

An agenda item has been included which is an integral part of every Board meeting, for

“discussion among Non-Executive Directors” (without the presence of the Executive Director) so

as to enable them to bring up any issue that needs to be highlighted.

(g) Encourage critical and constructive discussions at Board meetings

Compliant

All Directors are encouraged to make critical and constructive discussions at the Board

meetings and dissenting views are well received.

(h) The Chairman not to engage in executive functions

Compliant

The Chairman is a Non-Executive Director and does not supervise any management personnel of

the Bank directly.

(i) Communication with shareholders

Compliant

The Chairman has assigned the CEO to maintain a dialogue with institutional investors and to

bring any matters of concern to the notice of the Board.

The Investor Relations and Shareholder Communication Policy approved by the Board includes a

provision for communication with shareholders.

5.4

Conduct of CEO

(a) CEO to be in charge of the management of operations and business

Compliant

The CEO is the head of the management team and is in charge of the day-to-day management of

the Bank’s operations and business.

At the beginning of the year, the Board discussed the Strategic Plan with the CEO and the Senior

Management, and agreed on the financial and non-financial targets to be achieved and action

plans to be implemented by the Bank. Progress is monitored on a regular basis, and the

assessment of the performance of the Bank is carried out by the Board at the end of the year

based on the initiatives laid down in the Strategic Plan.

(b) CEO not to be appointed/nominated as an employee/Director of another Bank or company

except as a Non-Executive Director of a subsidiary or associate company of the Bank

Compliant

The CEO complies with these requirements.

(c) CEO to ensure effective discharge of responsibilities as CEO, in the event he is

appointed as a Non-Executive Director of a subsidiary or associate

Compliant

5.5

Suitability of CEO

Compliant

The CEO is a fit and proper person in terms of the Banking Act and possesses sufficient

knowledge and experience in banking functions.

6.

Board Committees

Compliant

The Board has appointed the five Committees required by the direction.

6.1

Requirement for Board Committees

(a) Committees to report directly to the Board

Compliant

All Committees report directly to the Board.

(b) Authority of each Committee

Compliant

The Board-approved Terms of Reference of each Committee sets out the authority of the

respective committee.

(c) Board-approved Terms of Reference (TOR)

Compliant

All Committees are guided by the Board-approved Terms of Reference.

(d) Secretary for each Committee

Compliant

All Committees have a designated Secretary and minutes of all meetings are submitted to the

Board.

(e) Quorum for each Committee

Compliant

Quorum for each meeting consists of at least half of the Committee members.

(f) Report on performance of each Committee

Compliant

The reports on the duties, performance, and roles are published in the Annual Report.

6.2

Audit Committee

Please refer page 277.

(a) Chair of the Committee

Compliant

The Committee is chaired by an Independent Director who is neither the Chairman of the Board

nor any other Board Committees. The Chair of the Audit Committee is a qualified Chartered

Accountant.

(b) and (c) Composition of the members

Compliant

All members of the Committee are Independent Non-Executive Directors and possess a collective

balance of skills and expert knowledge in finance, accounting and auditing.

Majority of the members of the Committee are not members of the Risk Committee.

(d) External Auditor

Compliant

The Committee assists the Board in implementing a transparent process in the engagement and

remuneration of the External Auditor, and assists in the general oversight of financial

reporting, internal controls, and compliance with laws, regulations, and Codes of Conduct.

The Committee will ensure that the engagement of the External Auditor does not exceed six years

and the engagement of the audit partner does not exceed three years.

(e) Independence and effectiveness of the audit process

Compliant

The Committee reviewed the statement issued by the External Auditor pursuant to Section 163

(3) of the Companies Act No. 07 of 2007.

The Committee discussed the nature and scope of the audit with the External Auditor, and the

effectiveness of the audit process in respect of the financial year 2025.

(f) Non-audit services

Compliant

A formal policy approved by the Board on engagement of the External Auditor to perform

non-audit services is in place.

(g) Nature and scope of the external audit

Compliant

The Committee met with the External Auditor to discuss and finalise the scope of the audit to

ensure that it is in compliance with guidelines issued by the Central Bank of Sri Lanka.

(h) Review of accounting policies/systems and internal control framework

Compliant

The Committee reviewed:

The quarterly and annual reviews conducted by Group Internal Audit to assess the adequacy

and effectiveness of the Internal Control System of the Bank.

The assurance reports provided by KPMG on the adequacy and effectiveness of the Bank’s

Internal Control System and Risk Management Framework, in compliance with applicable listing

rules.

(i) Review of financial information of the Bank

Compliant

The Committee reviewed all quarterly unaudited Interim Financial Statements and the Financial

Statements for the year ended 31 December 2025.

(j) Meetings with External Auditor

Compliant

The Committee met with the External Auditor on four occasions, and at three of those

meetings, without the presence of the CEO and KMP.

(k) Review of Management Letter

Compliant

The Committee considered the Management Letter issued by the External Auditor for the year

ended 31 December 2024 and the Management responses thereto.

GRI

2-19

2-20

Section

Governance principle

Compliance

Remarks

(l) Internal audit function

Compliant

The Committee reviews the adequacy of the internal audit function to ensure that it conforms

with the Audit Committee Charter. The annual audit plan is approved by the Committee. The plan

covers the scope and resource requirements. The annual performance appraisal of the Head of

Internal Audit and the Senior Staff Members are reviewed by the Committee. The internal audit

function is Independent of the activities it audits and the findings are reported directly to

the Audit Committee.

(m) Internal audit findings

Compliant

The Committee reviewed the internal audit reports and considered the findings,

recommendations, and corrective action.

(n) Attendance of non-audit committee members

Compliant

Vice President, Head of Internal Audit attends all Committee meetings. CEO, DCEO, CFO, other

Heads of Units, and the External Auditor attend meetings on invitation. During the year, the

Committee met with the External Auditor on three occasions without the presence of the Executive

Director.

(o) Terms of Reference

Compliant

The Committee is guided by the Audit Committee Charter.

(p) Meetings

Compliant

During the financial year ended 31 December 2025, ten meetings were held.

Attendance of Committee members is given in the table on page 215.

(q) Secretary

Compliant

Vice President, Head of Internal Audit serves as the Secretary of the Committee.

(r) Whistle-blowing policy and fair and independent investigation

Compliant

The Board has adopted a Whistle-blowing Policy to encourage employees to communicate

legitimate concerns on any illegal or unethical practices.

Arrangements are in place for fair and independent investigations and follow-up action to be

carried out.

(s) Key representative body for External Auditor

Compliant

The Committee acts as the key representative body for overseeing the Bank’s relations with

the External Auditor.

6.3

Human Resources and Remuneration Committee

Please refer page 281.

(a) Chair of the Committee

Compliant

The Committee is chaired by an Independent Director who is not the Chair of the Board.

(b) Composition of members

Compliant

The Committee is constituted with a majority of Independent Directors.

(c) CEO’s presence

Compliant

The CEO attends meetings and participates in deliberations except when matters relating to

him are discussed.

(d) Remuneration policy

Compliant

A formal remuneration policy approved by the Board is in place.

(e) Goals and targets for CEO and KMP

Compliant

The Key Performance Indicators (KPIs), as defined in the Strategic Plan of the Bank, were

reviewed by the Board and the KPIs of the CEO and KMP are as per the Strategic Plan.

(f) Review of performance of CEO and KMP

Compliant

The Committee annually reviews the performance against the set targets of the CEO and other